| For the past five years, Connecticut Insurance Exchange, Ltd. has been welcoming players to the Newington Veteran Firefighter’s Association (NVFA) annual Golf Tournament as the tournament’s Platinum Sponsor. They provide delicious mini donuts and bagels, and a major raffle prize.  Connecticut Insurance Exchange President Ron Tregoning  Newington Veteran Firefighter’s Association volunteers registration table | This year, the tournament was held on Friday, June 9th at Stanley Golf Course in New Britain. Just before the shotgun start, Newington Veteran Firefighter’s Association (NVFA) Golf Committee Member Mike Iskra presented Connecticut Insurance Exchange President Ron Tregoning with a plaque thanking him for the many years of support. Iskra explained, “We’re very fortunate and thankful to have Connecticut Insurance Exchange supporting our event each year. We wanted to honor Ron and his staff with this plaque to show him how much we appreciate all they do for us and the community.” “When the NVFA Golf Committee approached me to become a Platinum Sponsor five years ago, it was easy to say yes,” commented Tregoning. “As a Newington business owner for 40 years, I believe it is important to give back to the community. The Newington Veteran Firefighter’s have done so much for our town. Connecticut Insurance Exchange is proud to support them.” The NVFA tournament raises funds for an annual Newington High School scholarship, which goes toward young men and women who choose a career in firefighting, and to minimize the costs associated to run events supporting Newington firefighter veterans. Connecticut Insurance Exchange, Ltd. — located at 112 Market Square in Newington — has been serving the insurance needs of over 5,000 individuals, families and businesses since 1977. |

|

9 Comments

Situations change. Time to ask yourself, 'do I have enough coverage?' Everyone is more than busy these days. However, it's a good idea to stop and re-assess your insurance coverage on a regular basis. That’s because coverage may very well need to be updated or changed to accommodate any life changes to fully protect you, your loved ones and your property. Consider this — if you aren't covered properly, the cost of a claim may come out of YOUR POCKET. That's why DIY, online insurance sites may seem to save you money. But in actuality can COST YOU MORE in claims... A LOT more... if you don't have high enough limits.  Here's an actual case straight out of the "penny-wise-pound-foolish" department:

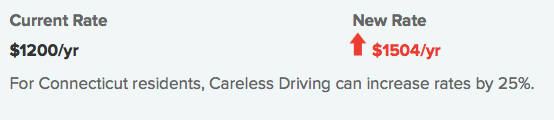

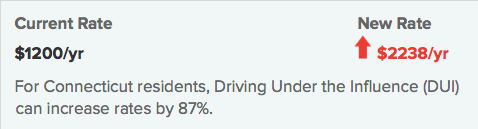

In 1984, while he was a captain in the U.S. Army, Charles Cohan purchased an automobile insurance policy from USAA with a $100,000 per-person liability limit. He kept the same coverage limits through 2011. He married Lisa Cohan in 1995 and added her to the auto policy as an “operator,” but never increased the liability limit. In 2002, the Cohans purchased land and built a new home. They purchased homeowner's insurance with liability coverage in the amount of $1 million per occurrence but did not purchase an umbrella policy. Lisa Cohan, while driving a Cohan vehicle, collided with another vehicle, killing the driver. A wrongful death suit was brought against the Cohans. The insurance company defended the action on Lisa's behalf. The matter settled for $300,000 but the insurance company paid only the policy limits of $100,000. The Cohans were responsible for paying the remainder of the settlement amount — $200,000! Got questions about policy limits? Don't be penny wise and pound foolish. Know your limits. Protect yourself, your loved ones, and your assets. Contact Connecticut Insurance Exchange at 860 666-5443 or info@cieltd.us for more information. We're always here to help!  A lot of drivers think that a receiving a moving violation such as tailgating, failing to yield the right of way or driving 15 mph over the speed limit is no big deal. Uh, wrong. In reality it could cost you quite a lot when it comes to auto insurance premiums. A recent study looks at how moving violations can impact insurance rates. These estimated findings may surprise some drivers...   The two most common reasons your auto insurance rate will increase is a traffic violation and and at-fault accident. While there's not much you can do after having an at-fault accident to improve your driving record (other than being more careful), there are a few things you can do to clean up your driving record.

How to clean your driving record

Where it lands is the key to liability...

Q: Let's say a neighbor's tree falls during a storm and crashes into your home. Who pays for the damage? This isn't meant to be a 'trick' question, but it may seem like one. A: Even though it's your neighbor's tree, it's your responsibility. If the tree was in good health and it came down due to an act of God, nobody can be held responsible for that. Tree damage — who pays for what?

There's a lot more to a home remodeling project than the price of the job. If you’re planning to do the work yourself or hire a general contractor (GC) or subcontractors, your FIRST CALL should be to your insurance agent to make sure you are adequately insured during the renovation and after it is completed.

Here are five 'what ifs' you may need to know BEFORE you begin… 1. What if the project can't be finished? After you’ve selected a GC — but before you sign a contract for the project — be sure the GC is licensed and bonded. If they can’t finish the job for some reason (such as illness or bankruptcy), the bond is intended to provide coverage for financial losses you may incur in getting the job finished. Your contract with the GC also should agree all work that is to be done is in accordance with current building codes and all permits will be obtained. Request a copy of your contractor's Certificate of Insurance. Check its effective and expiration dates to see if the coverage will be in force the entire time work is being done. Contact the insurance agency that issued the certificate if you have questions about coverage. 2. What if materials or equipment are stolen from my project? In general, building materials and equipment belong to the GC or subcontractors are NOT protected from theft by your homeowner's policy. A Builder's Risk Policy can be tailored to cover any of the contractor's equipment or materials that are left on your property to be installed. EXAMPLE: with the high cost of copper, thieves target construction sites looking for copper plumbing pipe. You should consider the purchase of a Builders Risk Policy for the length of YOUR renovation project. Be prepared. Determining the proper coverage and policy may require several conversations with your insurance agent as well as lenders, but is well worth the effort. 3. What if a subcontractor gets injured at my home? Confirm if your subcontractors carry Workers’ Compensation coverage of their own or are covered under the GC’s policy. If not and a subcontractor is injured on the job at your home, YOU could liable for injuries! 4. What if policy limits are inadequate? General Liability limits vary, but most GCs carry a $1 million limit. This amount may not be enough to cover damages. As the homeowner, you should consider adding additional limits with the purchase of an umbrella policy. 5. How much more is your home worth AFTER the renovation? Remember to speak with your insurance agent about increasing coverage for the NEW value of your property after it’s been remodeled. Got questions about your upcoming home renovation project? We're here to help! Connecticut Insurance Exchange offers a full line of insurance products, including Builder's Risk and Umbrella policies. Contact us at 860 666-5443 or info@cieltd.us to see how we may be able to assist you. According to the Bureau of Justice Statistics (BJS), an estimated 17.6 million persons, or about 7 percent of U.S. residents were victims of at least one incident of identity theft in 2014.

Once cybercriminals have access, they can steal personal and financial information, hold computer files for ransom, and hijack anything from webcams and thermostats to smart TVs! Here are tips from Ready.gov for what to do to prevent and manage a cyber attack. Protect your online profile

What you can do if you are experiencing an online breach

If you think your personally identifiable information (PII) is compromised

Ask a Connecticut Insurance Exchange agent about Identity Theft insurance. It's relatively inexpensive and could save you a lot of time and grief in the long run. |

News you can use from Connecticut Insurance Exchange covering topics ranging from your home, auto, business, liability and more.

AuthorMelanie Thomson-Tregoning is a Licensed Insurance Agent and VP of Marketing for Connecticut Insurance Exchange, Ltd. Categories

All

Archives

August 2023

|

RSS Feed

RSS Feed