A lot of drivers think that a receiving a moving violation such as tailgating, failing to yield the right of way or driving 15 mph over the speed limit is no big deal.

Uh, wrong.

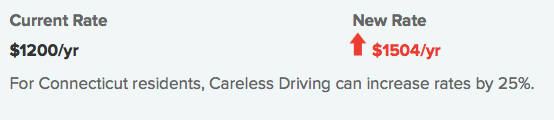

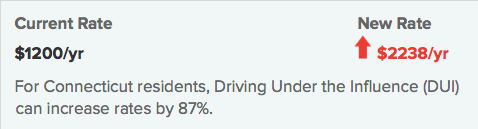

In reality it could cost you quite a lot when it comes to auto insurance premiums. A recent study looks at how moving violations can impact insurance rates. These estimated findings may surprise some drivers...

Uh, wrong.

In reality it could cost you quite a lot when it comes to auto insurance premiums. A recent study looks at how moving violations can impact insurance rates. These estimated findings may surprise some drivers...

The two most common reasons your auto insurance rate will increase is a traffic violation and and at-fault accident. While there's not much you can do after having an at-fault accident to improve your driving record (other than being more careful), there are a few things you can do to clean up your driving record.

How to clean your driving record

How to clean your driving record

- First, resolve to fight tickets if you think they are questionable. This will require a court visit. However, getting a violation dropped could you save you from a rate increase. But pick your battles — make sure the violations really are questionable. Mention any special circumstances. For instance, a judge might give you a break if you were rushing to the hospital because of an emergency.

- You may be able to take a defensive driving course to improve your auto insurance rate. Ask your CIE agent for details and availability.

RSS Feed

RSS Feed